Bond Market on Edge as Yields Rise Amid Tariffs, | Bonds & Fixed Income

Bonds I: Kerfuffle. Bloomberg reported that JPMorgan Chase & Co. CEO Jamie Dimon stated on the company’s Friday earnings call: “There will be a kerfuffle in the Treasury markets because of all the rules and regulations. When that happens, the Fed will step in—but not until ‘they start to panic a little bit.’ He added, ‘When you have a lot of volatile markets and very wide spreads and low liquidity in Treasuries, it affects all other capital markets. That’s the reason to do it, not as a favor to the banks.’”

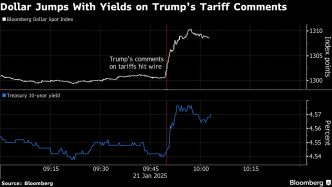

There has already been a kerfuffle within the bond market since April 2, i.e., on President Donald Trump’s self-proclaimed “Liberation Day,” when he introduced higher-than-expected reciprocal tariffs on 60 nations, together with an island populated solely by penguins. The tariffs have been scheduled to take impact on April 9, once they have been postponed for 90 days as a result of of the bond market’s kerfuffle. The tariffs on China, nonetheless, have been applied. The 25% tariff on aluminum, metal, and autos remained in place.

Trump acknowledged that he postponed the tariffs as a result of of the bond market’s kerfuffle. The bond yield did fall barely during April 3 and April 4 to 4.01%. But then it climbed to 4.49% on Friday, April 11. That occurred regardless of lower-than-expected March (CPI) and (PPI) readings on April 10 and April 11. Even the sharp drop in client sentiment during the primary two weeks of April (reported on April 11) didn’t stop the bond yield from transferring increased, as it will have in regular occasions.

The downside is that Trump’s Tariff Turmoil (TTT) is predicted to be inflationary, as evidenced by the massive leap in customers’ inflationary expectations during the primary two weeks of April. This implies that rising inflation seemingly would delay any easing to avert a recession. Fed officers aren’t about to decrease the federal funds price (FFR) anytime quickly, as they’ve been saying because the starting of the 12 months. In an April 4 , Fed Chair Jerome Powell prompt that they’re in even much less of a hurry to take action now than earlier than TTT, because the tariffs turned out to be increased than broadly anticipated:

“While uncertainty remains elevated, it is now becoming clear that the tariff increases will be significantly larger than expected. The same is likely to be true of the economic effects, which will include higher inflation and slower growth. The size and duration of these effects remain uncertain. While tariffs are highly likely to generate at least a temporary rise in inflation, it is also possible that the effects could be more persistent. Avoiding that outcome would depend on keeping longer-term inflation expectations well anchored, on the size of the effects, and on how long it takes for them to pass through fully to prices. Our obligation is to keep longer-term inflation expectations well anchored and to make certain that a one-time increase in the price level does not become an ongoing inflation problem.”

So bond buyers could also be in no rush to buy bonds, particularly since they might not be satisfied that Washington will do enough to scale back the federal deficit.

On Friday and Saturday, Trump continued to back off from his tariffs, which he has described as “a beautiful thing.”

Bonds II: The Yellen/Bessent Short-Term Solution to Debt. I’ve been on Wall Street for more than 45 years. Over that period, there was a lot of concern about mounting federal deficits and debt. Along the way in which, some of us bond market watchers noticed that bond yields tended to say no when federal finances deficits widened during recessions; that’s as a result of recessions brought on the federal authorities’s revenues to say no, as Americans’ incomes and earnings fell, and the federal government’s outlays to be boosted by its income help applications. Deficits have been principally counter-cyclical, widening during recessions and narrowing during expansions. No large deal.

Yet beginning within the Nineteen Eighties, there have been mounting considerations that federal authorities debt was rising relative to nominal GDP as deficits continued even during intervals of financial growth.

Lots of articles and books have been written because the Nineteen Eighties concerning the seemingly horrible penalties of a lot authorities debt rising so quickly. Stock and bond market bears typically included the federal deficits and debt of their litany of causes to be cautious. I tended to be principally bullish on stocks and bonds previously. With regards to federal authorities deficits and debt, I argued that I’d fear about them when the bond market apprehensive about them.

I did briefly fear in 2023, when the 10-year Treasury bond yield jumped from 4.00% on August 9 to five.00% on October 19. This resulted from bond buyers’ response to a collection of Treasury public sale measurement will increase beginning in August 2023, with quarterly refunding auctions for , 10-year, and maturities reaching $125 billion. These poorly obtained auctions heightened fears that a debt disaster was imminent. The bond market was choking on the availability of bonds, forcing yields up to ranges that would trigger a recession.

On November 1, 2023, the US Treasury, beneath Treasury Secretary Janet Yellen, introduced a discount within the tempo of will increase for longer-dated Treasury securities, easing the availability of new bonds. Yellen’s strategy leaned closely on issuing short-term Treasury payments to fulfill borrowing wants. The Treasury Borrowing Advisory Committee, which advises the Treasury Department on issues associated to the issuance of federal securities, has been recommending that no more than 20% of the Treasury’s marketable debt must be held in Treasury payments. Yellen took the ratio up to 22%.

This tactic was criticized by some, together with present Treasury Secretary Scott Bessent, for doubtlessly maintaining borrowing prices artificially low forward of the 2024 election. When Bessent took over as Treasury secretary in early 2025, he initially criticized Yellen’s method, arguing it shortened debt maturities an excessive amount of and clashed with the Federal Reserve’s inflation objectives. However, on February 5, 2025, the Treasury beneath Bessent introduced that it will preserve Yellen’s steering, maintaining longer-term debt issuance unchanged at $125 billion for quarterly refunding auctions spanning 3-, 10-, and 30-year maturities, with no will increase anticipated for “at least the next several quarters.”

“He and I are focused on the 10-year Treasury,” Bessent stated in a February 5 interview with F Business when requested about whether or not President Trump desires decrease rates of interest. “He is not calling for the Fed to lower rates.”

Bessent defined his continuation of Yellen’s plan in a February 20, 2025, Bloomberg Television interview, stating that any shift to Treasury’s issuing new debt with longer maturities was “a long way off” because of market situations, inflation, and the Fed’s quantitative tightening. He prompt a gradual method, as flooding the market with long-term bonds might spike yields and borrowing price.

I can’t be shocked if Bessent addresses the latest turmoil within the Treasury bond market by decreasing the dimensions of Treasury bond auctions, thus financing even more of the deficit with Treasury payments. The subsequent quarterly refunding announcement is scheduled for April 30. That would definitely push bond yields decrease. In impact, this is able to quantity to a coverage of Yield Curve Control by the Treasury (YCC-T) somewhat than the Fed (YCC-F).

As a thought experiment, what if the Treasury issued solely Treasury payments? The Fed could be pressured to buy a important quantity (if not all) of them to keep the FFR from rising above its vary. Bond yields would fall dramatically except inflationary pressures resulted, wherein case the Fed must raise the FFR vary. That would instantly increase the price of financing the Treasury’s debt. Might that put stress on Congress and the White House to scale back the deficits? Probably not, as a result of YCC-T would successfully bury the Bond Vigilantes.

Bonds III: Staying Vigilant. Since the beginning of this 12 months, I’ve been arguing that the 10-year US Treasury bond yield has normalized and is more likely to trade in a vary of 4.25%-4.75% for the remainder of this 12 months. I flinched after Liberation Day and lowered the vary to three.75%-4.25%. But now, I’m raising it back to 4.25%-4.75%, which is the place the bond yield principally traded within the years simply earlier than the Great Financial Crisis.

So the latest increase within the yield doesn’t faze me. But it has fazed heaps of different market observers. Indeed, I’ve been fielding heaps of calls from financial market journalists questioning whether or not the Bond Vigilantes are back on the scene. The reply is “no” if the bond yield merely has normalized. Then again, the latest leap in yields has been fast and livid, suggesting that the Bond Vigilantes are back and that on Wednesday of final week they pressured the Trump administration to postpone imposing reciprocal tariffs on quite a few nations across the world for 90 days.

The Bond Vigilantes are rightly involved that Trump’s Nitro Tariffs (TNT) will trigger an explosive increase in inflation. They are additionally involved that the latest weak point within the greenback means that foreigners are promoting their US bonds. And the Bond Vigilantes may be signaling that they aren’t satisfied that the Trump administration will rein within the federal deficit.

The good news is that Treasury Secretary Bessent appears to have satisfied President Trump that they shouldn’t mess with the Bond Vigilantes. On Wednesday, April 9, after ratcheting back all reciprocal tariffs to 10% for no less than 90 days (however upping the stress on China with a 145% tariff), Trump stated: “I was watching the bond market. The bond market is very tricky, I was watching it. But if you look at it now it’s beautiful. The bond market right now is beautiful. I saw last night where people were getting a little queasy.”

Trump additionally stated he listened to JPMorgan (NYSE:) CEO Jamie Dimon’s interview final Wednesday with Fox’s Maria Bartiromo, wherein Dimon stated a recession was seemingly and the bond market was sending unhealthy indicators about stress within the financial plumbing.

President Bill Clinton had a related epiphany in 1993 after his advisor James Carville stated: “I used to think that if there was reincarnation, I wanted to come back as the President or the Pope or as a .400 baseball hitter. But now I would like to come back as the bond market. You can intimidate everybody.”

Bonds IV: Supply & Demand. Everyone in our business appears to be questioning why the 10-year Treasury bond yield has been rising in latest days.

The broadly accepted view is that hedge funds needed to unwind foundation trades by promoting bonds when the yield turned unstable in response to TNT. But additionally among the many ordinary roundup of suspects is the Chinese authorities, which may be promoting Treasuries in retaliation towards Trump’s 145% tariff on items imported from China.

Reporter Jon Sindreu got here up with a intelligent rationalization in an article posted by The Wall Street Journal on April 11 titled “The Simple Explanation for This Week’s Treasury Market Mayhem.” He wrote: “But the answer might be far simpler: U.S. government debt is doing badly because, well, investors don’t want to buy it.” In different phrases, bond yields are rising as a result of there are fewer consumers than sellers of US Treasury bonds.

Consider the next:

(1) The largest vendor of these bonds, of course, is the US Treasury. Yet Reuters reported on April 9: “A U.S. Treasury debt auction of $39 billion in benchmark 10-year notes was well received on Wednesday, showing solid investor demand even after a bond market sell-off driven by an escalating trade war between the United States and its major trading partners led by China. The U.S. Treasury’s auction came in better than expected, priced at a high yield of 4.435%, lower than the rate forecast at the bid deadline.” Indirect consumers, a class that usually consists of overseas central banks and personal buyers, purchased 87.9% of the availability allotted to them, above the average of 70%.

(2) March’s CPI and PPI inflation charges have been decrease than anticipated, we realized when launched on Thursday and Friday. Yet the bond market wasn’t impressed. That’s as a result of on Thursday, the Treasury Department reported that the federal deficit was $2.1 trillion over the 12 months via March, and on Friday the Survey Research Center reported that the Consumer Sentiment Survey confirmed that buyers’ year-ahead anticipated inflation had soared to six.7% final month, the best price recorded since 1981.

(3) Bessent ought to clarify to the President that the steadiness of funds all the time balances. The flip aspect of America’s present account deficit are web capital inflows.

So for instance, final 12 months, the previous totaled $1.13 trillion, whereas the latter totaled $1.26 trillion. This means that if Trump succeeds in decreasing the trade deficit, foreigners may have fewer {dollars} with which to buy US Treasuries and different securities.

Original Post

Stay up to date with the latest news within the finance markets! Our web site is your go-to source for cutting-edge finance news, market trends, insights, and updates on key sources. We present every day updates to make sure you have entry to the freshest data on commodity actions, industry efficiency, provide and demand shifts, and main market bulletins.

Explore how these trends are shaping the long run of international commodities! Visit us often for essentially the most partaking and informative content material by clicking right here. Our fastidiously curated articles will keep you knowledgeable on market shifts, investment methods, commodity evaluation, and pivotal moments within the world of sources.